Investing Basics 101: 3 Essential Guidelines for Asset Allocation

Asset allocation is one of the first decisions to need to make when building a portfolio that suits your needs and goals; when you need the money essentially dictates where to invest it.

As such, there’s no one-size-fits-all solution. Asset allocation should depend on factors such as age, income, risk tolerance, financial needs, and goals.

As a general rule, money that you need in the near to mid-term should be held in cash and safe assets, respectively. On the other hand, money that is not needed over the next five years is a great candidate for the stock market, in general, as it tends to outperform other asset classes over a longer time frame.

Here, there are some general rules that you can follow when deciding how to allocate your assets. By the way, I use this framework myself.

Guideline 1: Money that you need in the next six months should be held in cash

Although all the guidelines I list here are going to be important, this is perhaps the most important of all. The last thing you want is to be forced to liquidate your stocks during a market downturn and incur a loss on your investment.

As such, any money that you will need to spend over the next six months should be held in cash. I think it may be even prudent to be a bit more conservative and have at least one year’s worth of expenses in cash. You can keep your cash in a high-interest account so you can benefit from the higher interest rate.

Guideline 2: Money that you need over the mid-term should be held in safe, less volatile assets

You don’t want to dabble in volatile assets for the money you need in the next three to five years.

This portion of your savings should be held in safe assets such as government or high-quality corporate bonds or fixed deposits.

This can be achieved either by buying individual bonds (the investment amounts tend to be quite high) or through a bond ETF. Some ETFs including those offered by Vanguard have a range of options from “Total Bond Market Index”, “Total Corporate Bond ETF” and many other variations. Similarly, iShares also offers bond ETF solutions together with other ETF providers.

For individual bonds, the advantage of bonds is that you can hold them to maturity, and you will not have to worry about fluctuations in the bond price. You can also choose bonds that have a maturity that suit your investment time frame. Also, you will benefit from the regular coupon payments you receive from your bond investment which you can use. As for ETFs, the ETF provider will take care of buying and selling the bonds, as an investor you need to ensure that the bond ETF you are buying is well-managed and has sufficient liquidity so it's easy for you to sell your holdings if required.

You should not be investing this portion of your portfolio in stocks as it can be quite volatile in the short term. Ideally, your investment horizon for stocks should be longer than five years.

Guideline 3: Money you don’t need for more than five years can (and should) be invested in stocks

The last bracket of money is that which you don’t need for more than five years. This money is the perfect candidate for shares.

Even if you are retired, a portion of your wealth should be invested for the long term. That’s because life expectancy has increased substantially. It is estimated that a 65-year-old retiree is expected to live another 22 years.

Stocks have historically outperformed all asset classes over a long-time frame. The average annualized return for the S&P 500 since its inception in 1928 through Dec. 31, 2021, is 11.82%.

According to Jeremy Siegel’s book, “Stocks for the Long Run”, stocks beat bonds 71% of the time in rolling five-year periods, 80% of the time in rolling 10-year periods, and 100% of the time in rolling 30-year periods.

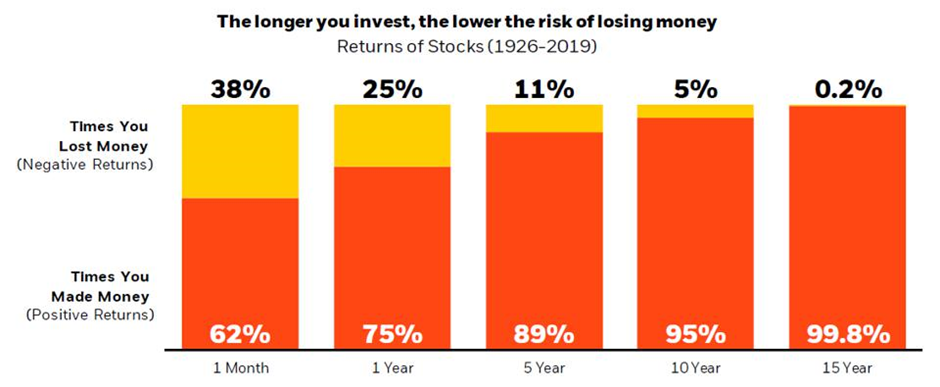

The chart below also perfectly illustrates why long-term investing in stocks is a great option, even for “risk-averse” investors.

The chart shows the odds of making losses in the US market represented by the S&P 500 index from 1926 to 2019 for different holding periods.

Although the chart shows that there is about a 40% chance of losing money over one month, the odds of making a loss drop substantially if your holding period is 10 years or more.

That just goes to show that a so-called “risky asset” has very limited risk if held over the long term. Coupled with its better track record of returns, stocks are a perfect investment over the long-term.

If you liked our article, subscribe to our newsletter to receive our latest articles directly in your inbox. The subscribe button can be found at the corner of the page.

Disclaimer: All opinions shared in this article are the opinions of the authors and do not constitute financial advice or recommendations to buy or sell. Please consult a financial advisor before you make any financial decisions. The authors do not hold positions in any of the mentioned securities.

Comments ()