Medtronic Deep Dive - The Awakening of a Sleeping Giant: Medtronic’s Strategic Pivot to Innovation-Driven Growth

I. The Premise: Assessing the Sleeping Giant

1.1. Introduction: Validating the "Awakening" Thesis

The term "Sleeping Giant" has historically applied to Medtronic plc (NYSE: MDT) due to its immense market capitalization, global footprint, and foundational role in health technology, often contrasted with periods of slower organic growth and operational complexity. The current investment thesis posits that this giant is now awakening, catalyzed by successful pipeline execution and strategic portfolio rationalization. This shift is not merely cyclical; it represents a structural pivot from managing integration complexity to aggressive, innovation-led commercialization.

Recent financial results provide quantitative evidence for this strategic resurgence. Medtronic reported strong second-quarter fiscal year 2026 financial results, which showed clear momentum across key enterprise growth drivers. In response to this outperformance in the first half of the fiscal year, management raised its full-year organic revenue growth guidance to approximately 5.5%, up from the prior projection of 5.0%. This acceleration is critically underpinned by a strategic spending shift: the company is channeling underlying efficiency gains in its gross margin toward future growth. Research and development (R&D) expenses increased substantially, rising 8.2% year-over-year to $754 million, matched by a 7.5% jump in selling, general, and administrative expenses. This simultaneous commitment to fueling the innovation pipeline and aggressively marketing new programs is the clearest quantitative signal that the organization has shifted its focus from cost-containment to market leadership.

1.2. A Legacy of Scale and the Covidien Complexity

Medtronic’s origins trace back to 1949, when electrical engineering student Earl Bakken and Palmer Hermundslie founded a small repair business focused on medical electronics. The company rapidly cemented its legacy in revolutionary health technology, pioneering the world’s first battery-operated pacemaker in 1957. Subsequent decades saw expansion into complex fields, including the establishment of deep brain stimulation (DBS) systems for movement disorders in collaboration with French doctors in 1987.

The scale of the company dramatically increased with the 2015 acquisition of Covidien. This transaction was transformative, expanding Medtronic’s reach into surgical devices, patient monitoring, and respiratory care, and significantly bolstering the Medical Surgical segment. The sheer size of the deal necessitated substantial external financing, which involved the commitment of $16 billion USD in external debt.

The period immediately following 2015 was characterized by significant internal focus on managing the consequences of this scale. The integration of Covidien was lengthy and complex, requiring substantial commitments of time and resources by both Medtronic and Covidien management, which inevitably diverted attention and capital away from purely organic growth opportunities. This necessary internal focus, combined with the burden of leveraging debt and regulatory setbacks in certain segments, contributed to the structural drag that justified the market’s perception of Medtronic as a "sleeping giant." Restructuring charges related to achieving cost synergies from the integration continued through the third quarter of fiscal year 2018. The current acceleration is structurally sound because the company appears to have finally absorbed the scale provided by Covidien and can now pivot its capital and strategic attention entirely toward disruptive external innovation, such as Pulsed Field Ablation (PFA) and Renal Denervation (RDN).

II. Mapping the Colossus: Segmentation and Financial Health

2.1. The Four Pillars: Segment Breakdown and Strategic Positioning

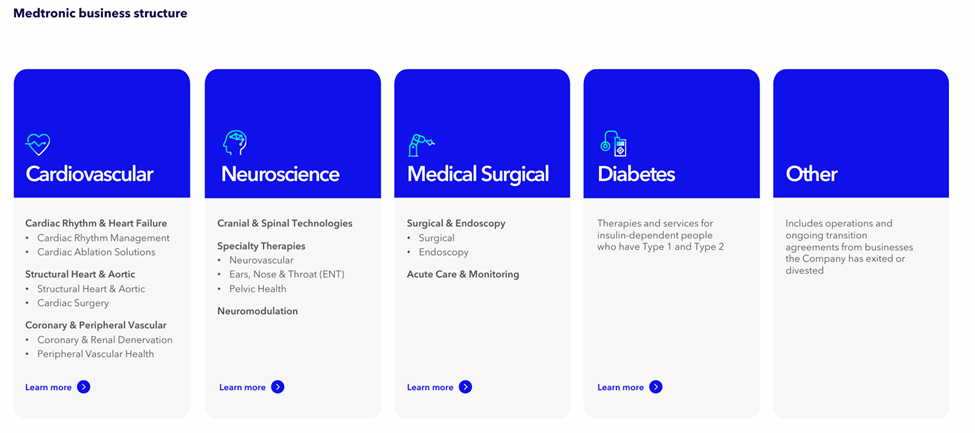

Medtronic’s operational model is built upon four primary business segments, enabling the company to offer solutions for over 70 distinct health conditions across more than 150 countries.

- Cardiovascular (high margin): The largest portfolio, generating $12.48 billion in fiscal year 2025 (37.2% of net sales). This portfolio encompasses Cardiac Ablation Solutions, Cardiac Rhythm Management (pacemakers, defibrillators), Structural Heart, and the newly commercialized Renal Denervation systems (Symplicity). It is currently the leading driver of the enterprise’s accelerated revenue growth.

- Neuroscience (high margin): Accounted for $9.85 billion in FY25 sales (29.4% of total), specializing in Cranial and Spinal Technologies, as well as neuromodulation for pain management, movement disorders (e.g., Deep Brain Stimulation) and Pelvic Health (Altaviva). This segment typically delivers durable, high-margin revenue streams due to the complexity and specialized nature of its implantable devices.

- Medical Surgical (low margin): Representing $8.42 billion in FY25 sales (25.1% of total), this segment includes surgical instrumentation, endoscopy, and acute care and monitoring.11 The products range from advanced surgical stapling, vessel sealing, and hernia repair devices to patient monitoring equipment like capnography and pulse oximetry monitors. This segment carries the lowest organic growth rate in the enterprise, highlighting its central role in the turnaround strategy and it currently serves as the primary target for revitalization via the Hugo™ robotic platform.

- Diabetes (margin dilutive): Accounted for $2.79 billion in FY25 sales (8.3% of total), focusing on integrated therapies and services, including insulin pumps and continuous glucose monitoring (CGM) systems, for people requiring intensive insulin management and is currently being prepared for separation as an independent entity.